Are you spending thousands on auto insurance lead generation without knowing which strategy actually works? You're not alone. Most insurance agents struggle between two options: running their own Google Ads campaigns or buying leads from third-party vendors.

The stakes are high. Google Ads for auto insurance can cost $40-$80 per click in competitive states. Meanwhile, shared leads from vendors often get sold to multiple agents, reducing your conversion rates dramatically.

Here's what makes this decision critical: Your customer acquisition cost directly impacts your business survival. Get it wrong, and you'll burn through marketing budgets with nothing to show.

This guide breaks down the real costs, conversion rates, and ROI data for both approaches. You'll learn which strategy fits your budget and goals, plus proven tactics to maximize results from either path.

Table of Contents

Google Ads for auto insurance work because people actively search when they need coverage. Someone typing "cheap auto insurance Phoenix AZ" is ready to buy today.

The challenge? High-volume terms like "auto insurance quotes" cost $40-$80 per click in California and Florida. That's brutal for smaller agencies sending traffic to generic homepages.

A solo agent should start with $500-$1,000 monthly for Google Ads. This covers 15-25 clicks per day in most markets. Larger agencies often spend $3,000+ monthly for meaningful market share.

Here's the math: PPC lead generators pay $15-$60+ per click. Only 5-15% of clicks complete lead forms. Raw lead generation costs reach $100-$1,200 per lead from paid search.

Target local and action-ready searches. Focus on these high-converting keyword types:

"Cheap auto insurance [city name]" - immediate price shoppers

"Auto insurance near me" - local intent with mobile traffic

"[State] car insurance rates" - comparison shoppers

"Auto insurance quotes online" - ready to compare options

"Car insurance discounts [city]" - price-sensitive prospects

Avoid broad terms like "how does car insurance work." These bring tire-kickers, not buyers.

Never send Google Ads traffic to your homepage. Create dedicated landing pages with:

Instant quote tools or lead capture forms

Local phone numbers and office addresses

Customer testimonials from your area

Clear value propositions about savings

Mobile-optimized design for smartphone users

The goal is capturing contact information immediately. Every extra click loses prospects to competitors.

Buying auto insurance leads offers immediate pipeline filling without managing campaigns. But not all leads are created equal.

The biggest mistake agents make? Going all-in on one lead source. When that source changes prices or dries up, your pipeline goes to zero overnight.

The 2026 insurance lead fraud report shows one in three leads from affiliate networks has problems. Common issues include:

Recycled leads sold multiple times

Fake contact information or invalid data

Prospects who never actually requested quotes

Leads generated through misleading advertising

Geographic mismatches for licensed agents

Always test new lead sources with small purchases first. Track contact rates, not just conversion rates.

Every auto insurance lead likely went to several agents simultaneously. The fastest response usually wins the sale.

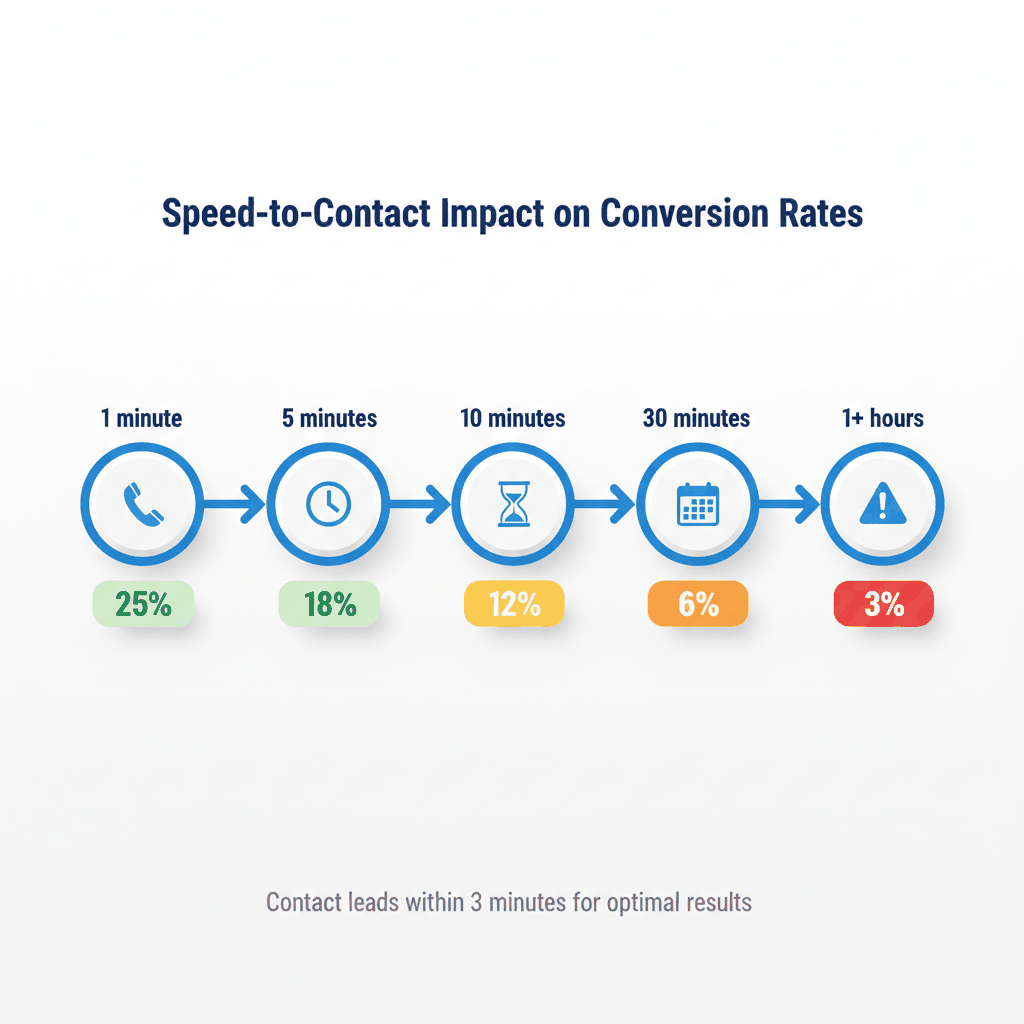

Contact ALL auto insurance leads within 3 minutes when possible. Auto insurance prospects submit multiple quote requests and work with the first agent providing competitive quotes.

Research shows 82% would drop brokers over slow response times. Speed-to-contact directly correlates with conversion rates.

This is the deadliest mistake in the industry. You contact someone, they aren't ready today, and you never talk again.

Here's the reality: 80% of sales happen between the 5th and 12th contact. If you aren't staying in front of prospects, competitors are.

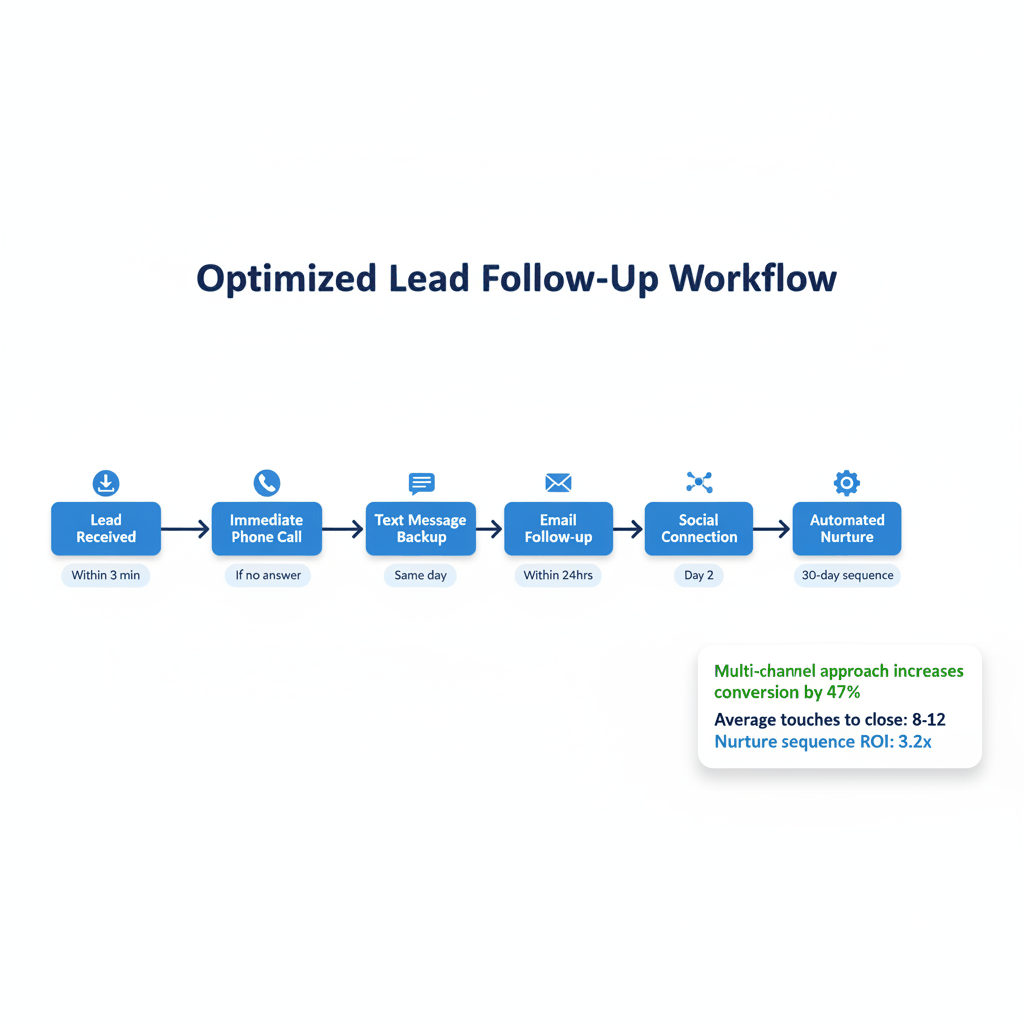

Build automated follow-up sequences that nurture leads over 30-90 days. Mix email, text, and phone outreach for maximum impact.

Understanding real lead costs helps you budget effectively and compare options accurately.

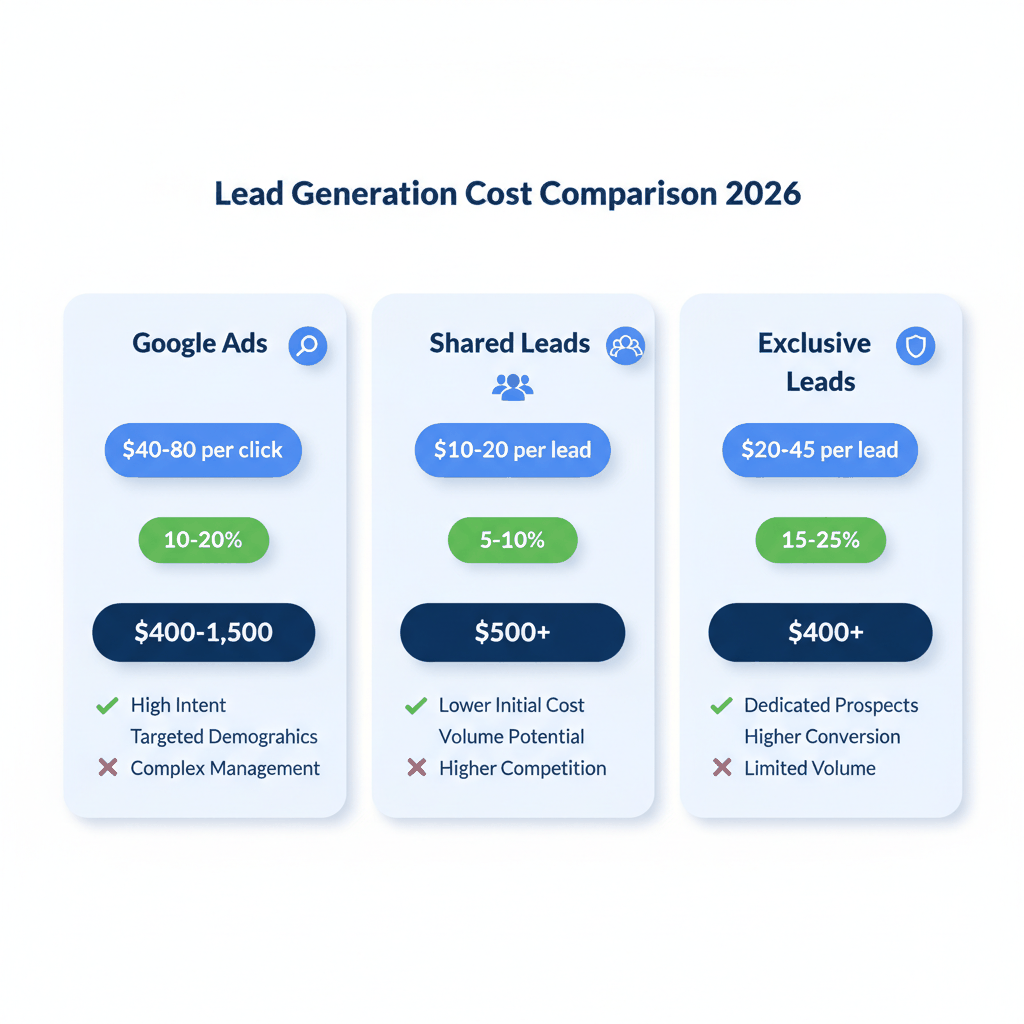

Shared leads typically cost $10-20 each. These leads get sold to 3-5 agents simultaneously, creating immediate competition.

The math often doesn't work. A shared lead at $25 converting at 5% costs $500 per customer acquired. Plus you're competing against multiple agents for the same prospect.

Exclusive leads range from $20-45 depending on qualification level. Higher upfront costs, but significantly better conversion rates.

An exclusive lead at $60 converting at 15% costs $400 per customer acquired. The exclusive lead is cheaper per acquisition despite higher per-lead costs.

Live transfer calls can reach $25-75 depending on qualification. You're connected directly with interested prospects who answered qualifying questions.

These represent the highest intent leads available. Conversion rates often reach 25-40% for skilled agents.

Search advertising costs per click range from $10-60+ for auto insurance terms in competitive markets. Add landing page creation, management time, and testing costs.

Total acquisition costs through Google Ads typically range $400-1,500 per customer, depending on market competition and campaign optimization.

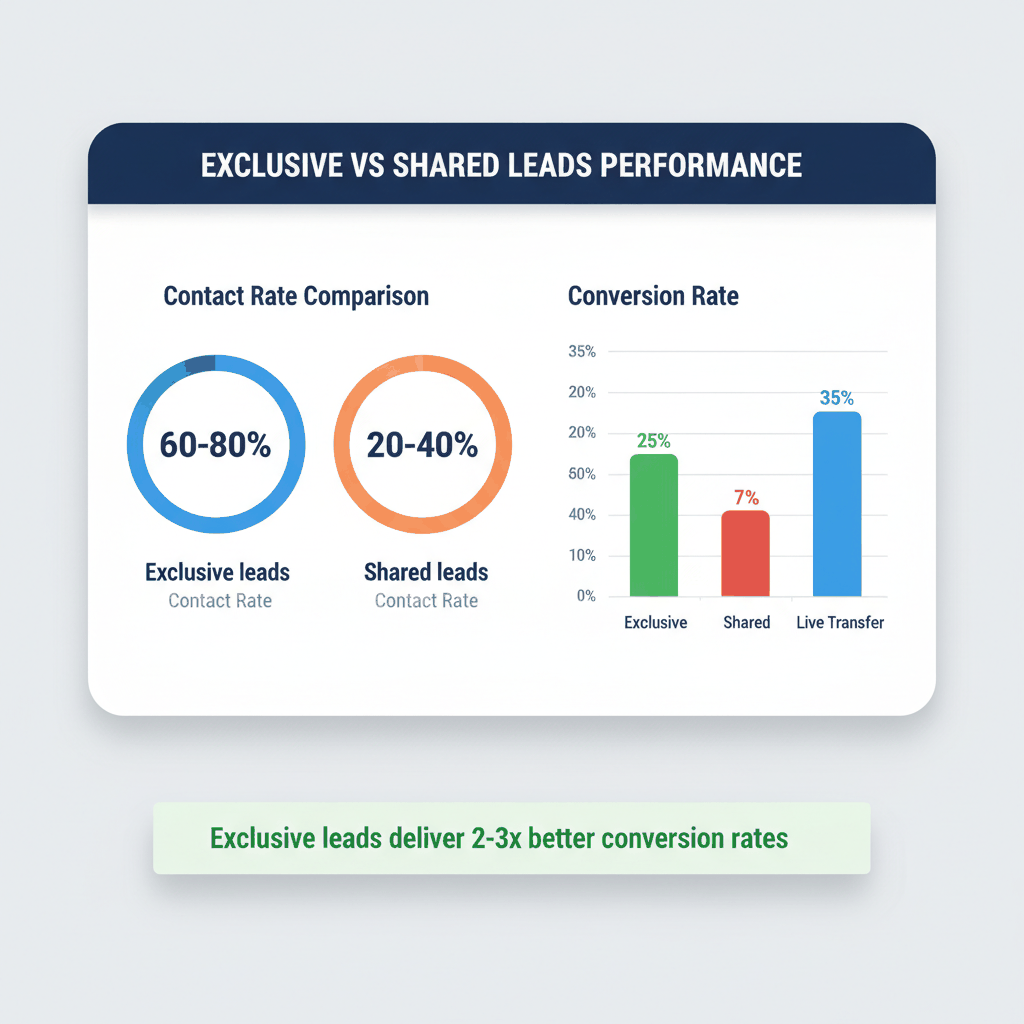

The choice between exclusive and shared leads dramatically impacts your ROI and sales team efficiency.

Exclusive auto insurance leads consistently deliver 60-80% contact rates. When prospects talk to one knowledgeable agent instead of fielding multiple calls, engagement improves dramatically.

Shared leads often show 20-40% contact rates. Prospects get overwhelmed by multiple agent calls and start ignoring unknown numbers.

For auto insurance, conversion rates vary significantly by lead source and exclusivity:

Shared leads: 5-10% conversion to bound policies

Exclusive leads: 15-25% conversion rates

Live transfers: 25-40% for experienced agents

Google Ads leads: 10-20% depending on landing page quality

Exclusive leads convert to bound policies at 2-3x the rate of shared leads consistently across agencies.

Exclusive leads typically close within 7-14 days of initial contact. Shared leads often take 30+ days as prospects compare multiple quotes and agents.

Shorter sales cycles mean faster commission payments and less pipeline management overhead for your team.

Sarah from a case study explained the transformation: "When we moved to exclusive leads, even though they cost more per lead, our agents started closing more business with less effort. It completely changed the energy in the office."

Agents prefer exclusive leads because they can focus on consultation rather than competing against multiple other agents on every prospect.

Maximizing ROI from any lead source requires systematic optimization of your sales process and follow-up systems.

Insurance-specific CRM systems outperform generic options for lead tracking and follow-up automation. Top options include:

AgencyBloc - Built for insurance agencies with policy tracking

Applied Epic - Comprehensive agency management system

Shape CRM - Insurance-focused with AI-powered lead scoring

HubSpot - All-in-one platform with strong automation

Modern CRM systems integrate with lead sources automatically, ensuring no prospects fall through cracks in your follow-up process.

Build follow-up sequences using multiple communication channels for maximum reach:

Immediate phone call within 3 minutes

Text message if no phone answer

Email with quote comparison tools

Social media connection on LinkedIn

Direct mail for high-value prospects

The goal is staying top-of-mind without being pushy or annoying to prospects.

Auto insurance clients represent prime opportunities for home, life, and umbrella coverage cross-selling. Clients with multiple policies show significantly higher retention rates and lifetime value.

This makes auto leads profitable even at break-even acquisition costs when you factor in additional policy sales over time.

Auto insurance pricing follows seasonal patterns. Prices increase in spring and early summer during peak moving seasons. Winter months often offer the best rates for consumers.

Adjust your lead generation budget and messaging to match these seasonal trends for maximum conversion rates.

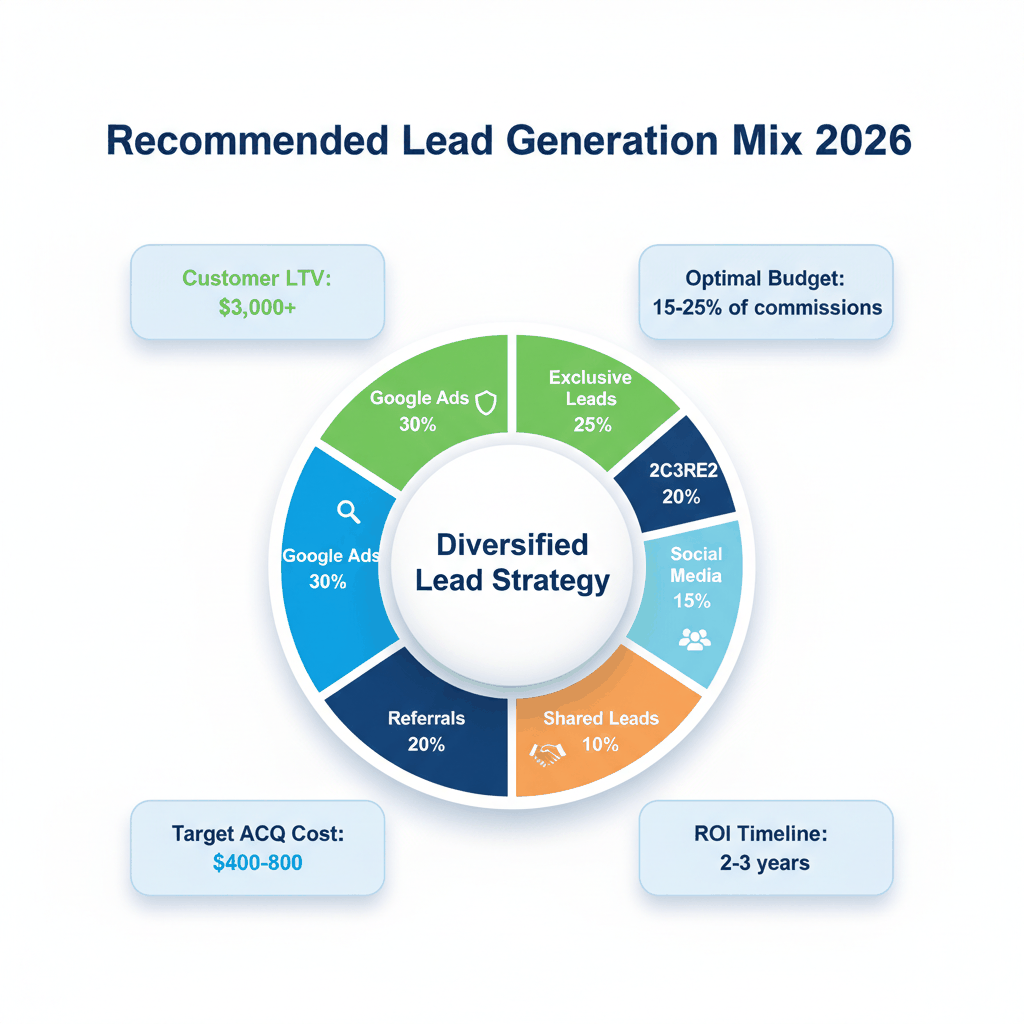

Making smart lead generation decisions requires understanding your true customer acquisition costs and lifetime value calculations.

Calculate your average customer lifetime value to determine appropriate acquisition spending:

Average annual premium: $1,200-2,400

Commission rate: 10-15% typically

Client retention: 2-3 years average

Cross-sell potential: 1.5-2.2 additional policies

A client worth $3,000+ in lifetime commissions justifies $400-800 acquisition costs comfortably.

Top-producing agents build lead generation stacks rather than relying on single sources. Recommended mix:

30% Google Ads (owned traffic)

25% Exclusive purchased leads

20% Referral systems and networking

15% Social media and content marketing

10% Shared leads for testing

This diversification protects against single-source dependency risks while optimizing costs across channels.

Track these metrics monthly to optimize your lead generation investment:

Cost per lead by source

Contact rates within 24 hours

Conversion rates to bound policies

Average time to close

Customer lifetime value by source

You can't optimize what you don't measure. Most agents guess which channels work instead of knowing for certain.

A 2022 case study generated nearly 3,000 verified conversions and 4,084 phone calls for $105,436 total investment. Average conversion cost was $35.23.

For most agencies, allocating 15-25% of gross commission income to lead generation provides sustainable growth without cash flow problems.

How much should I spend on auto insurance leads for sale monthly?

Most successful agents spend $500-2,000 monthly on auto insurance lead generation. Start with 15-20% of your gross commission income and adjust based on ROI performance. Track cost per acquisition rather than just lead costs.

Are exclusive auto insurance leads worth the higher cost?

Yes, exclusive leads consistently outperform shared leads despite higher upfront costs. An exclusive lead at $60 converting at 15% costs $400 per customer. A shared lead at $25 converting at 5% costs $500 per customer.

What's better for insurance agents: Google Ads or buying leads?

Both strategies work when executed properly. Google Ads provide more control and owned traffic but require ongoing management. Buying exclusive leads offers immediate pipeline filling with less hands-on work. Most successful agents use both.

How quickly should I contact auto insurance leads?

Contact auto insurance leads within 3 minutes when possible. Speed-to-contact directly impacts conversion rates since prospects typically submit multiple quote requests. The fastest response usually wins the sale.

What conversion rates should I expect from auto insurance lead generation?

Shared leads convert at 5-10%, exclusive leads at 15-25%, and live transfers at 25-40%. Your sales skills, follow-up system, and competitive pricing significantly impact these benchmarks.

Ready to get auto insurance leads? Sign up with ResultCalls today!

Hello everyone! My name is Alex and I write these blogs to help educate small business owners on different ways to grow their business. My goal is to make lead generation as easy as possible for you. After reading these blogs, I hope you leave with some actionable steps that will get you closer to growing your business :)